Welcome to my September 2023 Portfolio Report.

My stock portfolio fell in value by -£447.37 (-1.6%) across the month of September 2023. This figure excludes the benefit of any additional deposits made and focuses solely on return achieved on existing capital.

£0.00 additional deposits were pumped into the fund this month, £0.00 worth of stocks were sold, with £762.59 of total capital being invested into additional holdings. £36.37 in additional deposits were made due to income from dividends being transferred into the capital account. The additional deposits and dividend income minus the capital difference invested and account fees has therefore led to a decrease in the capital held on deposit which has fallen from £890.72 to £161.70

Capital held on deposit now sits at 0.6% of the value of the fund.

The total value of the fund, along with the cash held on deposit sits at £27,948.55

2023 Performance

On 1st January 2023 the account sat at a value of £22,630.27. Since then I’ve pumped in a further £2,165 into the fund. Today’s value of £27,948.55 minus the £2,165 additional deposits, means that I’ve made an investment return of £3,153.28 so far this year which represents +13.9% gain in value for the year.

My Thoughts

And so the portfolio fell -0.6% in value for September 2023 in a market where the FTSE 250 fell by -1.7% for the month. We are also well ahead for the year being up +13.9% versus the 250 which itself still sits at -4.5% for the year to date.

I didn’t add more capital this month purely because I didn’t get around to putting it in. So, sitting at £2,165 deposited in 2023 it means I’ll need to deposit another £800 over the final 3 months of the year in order to reach my £3,000 a year commitment. This should be easily achievable and I may even see myself go above that by year-end. Oddly (and this is pure coincidence) I only managed to deposit precisely £2,165 in 2022. I’ve no idea how I’ve found myself putting exactly that amount in again this year, but it means that I’m at a total deficit for the commitment I declared at the start of this journey and so any extra I can pump in this year to bring me back to where I should be overall will help get me back on track. The £3,000 reflects the £250/m commitment made when calculating my journey to £1,024,867.

The value of the fund has now dropped back below the previous high of Dec ‘21 (£28,192) and the more recent high last month of £28,395. It’s a shame, but I’ve written many times about my expectation that 2023 was always going to be a flat year. I felt like we didn’t deserve to expect much of a climb in value so soon. Inflation is still high, although calming. Interest rates are still higher, although peaking. Energy prices are still high, although falling. And yet despite that, the value of the portfolio is up +13.9% this year. I count that as a massive win should it stay there or thereabouts. Who knows when it comes to the markets. A few poor months and I could still see us down to breakeven by Xmas. Although I doubt this is likely now.

As I have always maintained, I believe it will be 2024, where we will start to see prices push higher. Assuming there’s no crash (which has been predicted as ‘imminent’ by many talking heads since 2021) I expect we’ll see inflation returning back closer to normality, interest rates coming back down a little, perhaps help for more first time buyers again, and energy prices continuing to reduce. If so, I suspect this contrast bias will lead to some sort of renewed confidence in stocks and a return to the markets for many investors, pushing prices up.

Many companies are reporting this year that the latest financials incorporate the impact of higher rates, and that the first quarter of the year ending 2024 has been more favourable for most. Suggesting 2024 may be a year of growth for many watchlist stocks. This all assumes no negative developments in Ukraine etc which is one of those events we neither have any control over, nor are we able to realistically forsee what might be coming.

Yet, despite all the forecasts and predictions, none of it really matters when focused upon the long term picture. If prices fall in 2024, I’ll be getting more shares for my money. If they rise, I’ll be getting less, but the ones I already own will be worth more. That’s the rub of it.

Last year I purchased £2,165 worth of shares over 12 months on the way down. This year, over the first 9 months, I’ve so far purchased £2,165 worth of shares on the way back up. That’s £4,330 worth of shares purchased at lower prices. To me, that’s where the real difference is made. When many investors ran from the markets, I got to work and carried on buying. My forecasts suggests that over 25 years, every £1 I invest will be worth £24 to me. If that turns out to be true, that £4,330 invested will be worth £103,920 to me one day.

Portfolio

| SHARES | STOCK | COST (£) | MARKET (£) | GAIN (£) | GAIN (%) |

|---|---|---|---|---|---|

| 120 | STOCK 1 | 877.62 | 1,186.80 | 309.18 | 35.22 |

| 1073 | STOCK 4 | 6,580.91 | 7,897.28 | 1,316.37 | 20.00 |

| 30 | STOCK 23 | 493.50 | 901.20 | 407.70 | 82.61 |

| 51 | STOCK 2 | 1,028.30 | 988.89 | -39.41 | -3.83 |

| 1902 | STOCK 25 | 2,584.60 | 2,225.34 | -359.26 | -13.90 |

| 1312 | STOCK 29 | 2,650.31 | 1,954.88 | -695.43 | -26.23 |

| 35 | STOCK 16 | 501.53 | 605.50 | 103.97 | 20.73 |

| 1505 | STOCK 32 | 1,269.04 | 1,173.90 | -95.14 | -7.49 |

| 110 | STOCK 34 | 1,557.70 | 1,510.30 | -47.40 | -3.04 |

| 13 | STOCK 17 | 248.05 | 650.26 | 402.21 | 162.15 |

| 2619 | STOCK 43 | 599.64 | 759.51 | 159.87 | 26.66 |

| 138 | STOCK 39 | 249.26 | 342.24 | 92.98 | 37.30 |

| 109 | STOCK 49 | 409.80 | 288.85 | -120.95 | -29.51 |

| 304 | STOCK 55 | 1,048.02 | 231.04 | -816.98 | -77.95 |

| 154 | STOCK 33 | 3,900.22 | 3,660.58 | -239.64 | -6.14 |

| 50 | STOCK 24 | 800.20 | 309.00 | -491.20 | -61.38 |

| 26 | STOCK 45 | 491.34 | 636.48 | 145.14 | 29.54 |

| 398 | STOCK 56 | 521.08 | 608.94 | 87.86 | 16.86 |

| 15 | STOCK 57 | 1,029.91 | 1,094.40 | 64.49 | 6.26 |

| 147 | STOCK 38 | 762.59 | 761.46 | -1.13 | -0.15 |

| TOTAL | 27,603.62 | 27,786.85 | 183.23 | 0.66 | |

| CASH | 161.70 | ||||

| TOTAL PORTFOLIO VALUE | 27,948.55 |

Dividend History

£36.37 was received this month in dividends and re-invested into the fund.

I have received a total of £659.62 in dividends so far for 2023 which is an average passive income of approximately £73 a month.

At the start of the year I explained I was hoping for a 2.5% yield from my account each year which would have amounted to £625 in 2023. So I have therefore achieved this already with 3 months left to go which is very pleasing. By this time last year I had received £646.44 in dividends. So we’re ahead of last years year to date total.

I will add, however, that having done some forecasting, it’s looking likely I may have to wait another year to reach that £1000/yr dividend milestone. The lack of special dividends being paid in 2023, in addition to no longer receiving Medica Group plc’s dividends after being sold due to the takeover, all leads to the suggestion we are likely to only make it to £900. Still somewhat leaps and bounds above the anticipated £625, and an improvement on 2022’s total of £836 if attained. So I certainly won’t be complaining.

2022 Dividend Income = £836.58

2021 Dividend Income = £681.58

2020 Dividend Income = £107.75

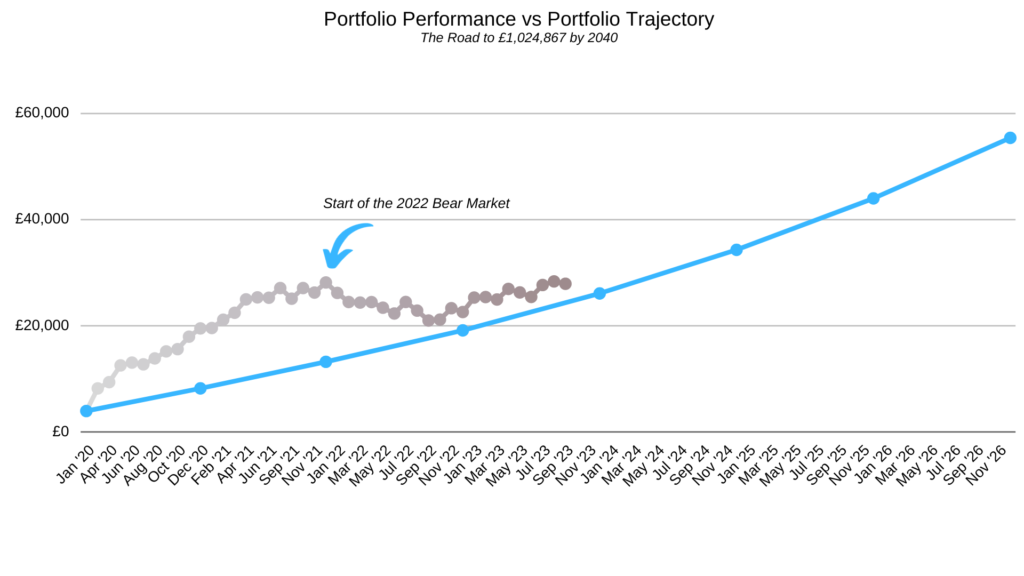

Historical Performance Tracker

My goal is to reach £1,024,864 in account value within 23 years from the start of this project. I plan to get there by achieving an average annual return of 15% from my stock picks and an additional average 2.5% annual dividend yield which will be re-invested into the fund for compounded growth. This also assumes a £250/month cash input to aid growth. This progress is represented as the blue ‘trajectory’ line.

My financial forecasts suggest that to stay on track and reach my goal I must finish 2022 on £19,169. By the end of 2023 I needed to be on £26,132.

The value of my fund has already reached almost £26,500 at this stage. As a result I am just ahead of schedule of reaching my target of £1,024,864 by 2042. This is despite the poor market returns of 2020-2023. However, my projections are already based on conversative returns, obtained from historical performance. I am therefore left in no doubt that I will make my target far sooner than planned. Initial projections suggested I would reach my end target aged 61. However, current projections now suggest the milestone will be reached by the age of 59. I hope to get there before I hit 55.

Join Me On My Journey

I hope you continue to join me for this rollercoaster ride across 2023 and our forthcoming years of financial growth. I sincerely hope to one day be able to meet some members in person and bask in each others stories of success. Nothing will please me more than for my hours and hours of analysis to have had significant positive impacts on peoples financial lives and welbeing. This is an incredible journey, growing a starter portfolio of £4k to £1 million. It will take best part of 20-25 years to achieve.

However, I hope these monthly reports then become a roadmap of sorts that future generations can take. I certainly intend for my children to take on the baton and continue running with it long after i’m gone. For me, this is a the start of the Chillingworth legacy. Whilst I started in my 30’s with less than £10k, my children will start in their 20’s with perhaps £100k each. Their children may start with a million each. Their children could eventually be billionaires. Whilst I won’t be around to witness it, I’d be happy knowing I came into and then left this world having made a positive impact to my family in this way.

The Podcast

If you haven’t yet checked out the Diary of a UK Stock Investor Podcast, you can do so by going to the Podcast page which provides all the links you’ll need to tune in. The Diary of a UK Stock Investor Podcast is a show for everyday retail investors. With a new episode every Thursday, we focus on successful investing in UK stocks discussing education, strategy, mindset, ideas and even stock picks and analysis. The show is curated by Chris Chillingworth, a UK investor for some 9 years whose stock picks have achieved a 16.8% annual average return between Jan 2014 – Jan 2023.